Housing Bust Update: It's Not Just the Cost of Buying, It's the Cost of Owning

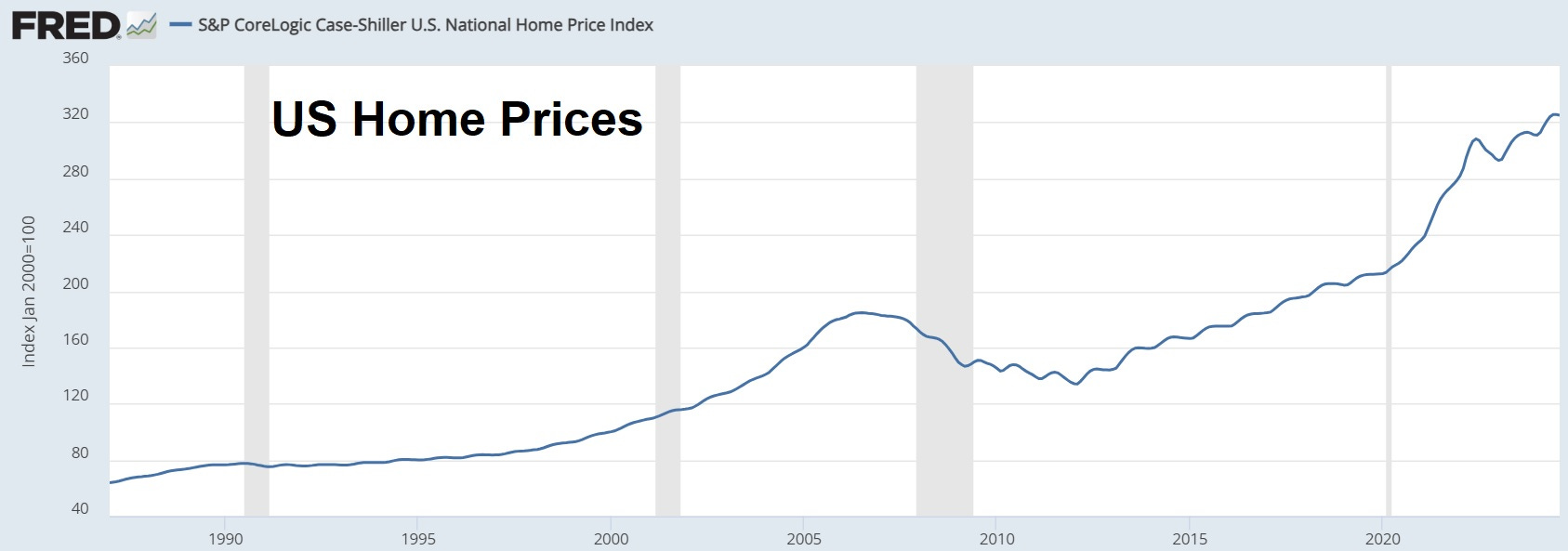

Home prices are at all-time highs, and — amazingly — are still rising. Compare today’s average price to that of 2007, which is generally thought to be the peak of America’s biggest-ever housing bubble:

And mortgage rates, which were supposed to fall when the Fed started easing in September, are instead rising. 7%, here we come.